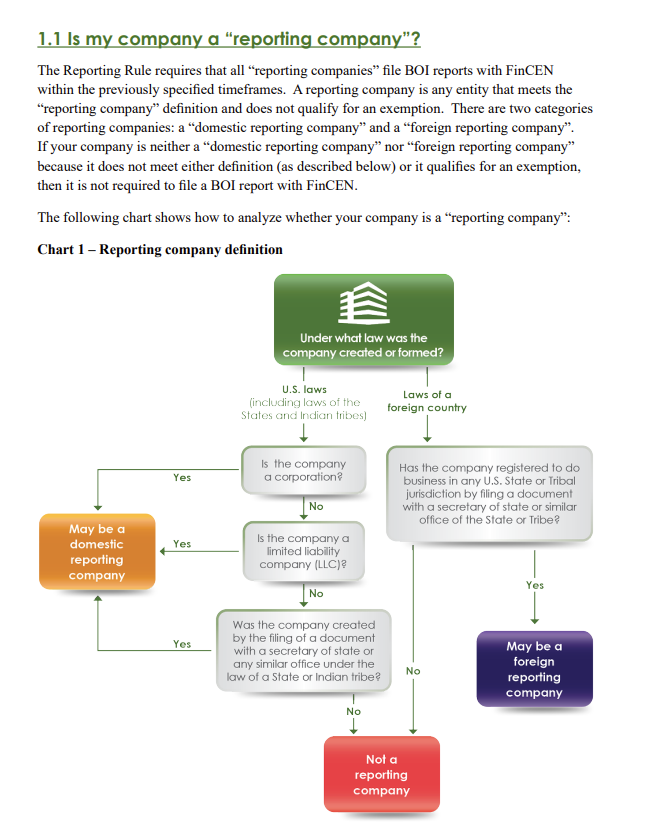

5 Key Factors That Influence Interest Calculation on a Car Loan

How to Calculate Interest on a Car Loan.

Taking out a car loan is a common practice for many people when purchasing a vehicle. Although the process of securing a car loan may seem straightforward, it’s important to understand how lenders calculate the interest on the loan. Understanding these 5 Key Factors that Influence Interest Calculation on a Car Loan will help you make a more informed financial decision and ensure that you are getting the best possible deal.

1. Interest Rates

Lenders provide financing to help borrowers purchase a new or used vehicle. The lender charges an interest rate, or a percentage of the loan amount, for borrowing the money. The interest rate varies among lenders and is influenced by factors such as your credit score, loan term, and prevailing market rates. Generally, borrowers with higher credit scores receive lower interest rates, while those with lower credit scores may receive higher rates.

2. Principal Amount

When you make a payment, a portion of that payment will go to paying the interest you owe that month, and the rest will go to paying your principal. The principal amount is the total amount of money borrowed for purchasing the car.

The interest calculation is based on this principal amount. As you make payments on the loan, the principal amount decreases, which affects the interest calculation over time. Keep in mind that a larger loan amount will result in higher interest charges, so it’s wise to consider making a substantial down payment to reduce the principal amount.

3. Loan Term

The loan term refers to the duration over which the loan is repaid. It typically ranges from 36 to 72 months, although longer loan terms are becoming more common. The loan term plays a significant role in interest calculation. Generally, a longer loan term means lower monthly payments but higher overall interest charges. Conversely, a shorter loan term may lead to higher monthly payments but lower total interest costs.

4. Amortization

Most car loans work like this: you make payments every month to cover both the amount you borrowed (the principal) and the interest charges. At the beginning of your loan term, most of your payments will go towards paying off the interest. But as time goes on, more and more of your payments will go towards reducing the actual amount you borrowed, or the principal amount. This is known as amortization, and it affects how much interest you have to pay.

It’s important to note that not all loans are the same. Some loans may have different payment structures, so it’s important to understand the terms of your specific loan.

5. Prepayment and Early Payoff

Some lenders may charge prepayment penalties if you choose to pay off your car loan early. These penalties are designed to compensate the lenders for potential interest income they would’ve made if you stuck to the original payment schedule.

If you’re thinking about making extra payments or paying off the loan early, be sure to understand whether any prepayment penalties apply. Evaluating the impact of prepayment penalties is essential when considering early repayment options.

Conclusion

Understanding how interest is calculated on a car loan is crucial for making informed financial decisions. By considering factors such as interest rates, principal amount, loan term, amortization, and prepayment options, you can better evaluate the total cost of the loan.

It’s always a good idea to compare offers from different lenders and carefully read the terms and conditions of the loan agreement before making a final decision. Armed with this knowledge, you can navigate the car loan process confidently and secure a loan that fits your needs while keeping interest costs as low as possible.

If you’d like more information on the car buying process, check out the COPFCU Car Buying Guide.

Related Content